Artificial Intelligence Becomes the Top Investment Priority

What You Should Know

- KLAS Research Global HIT Trends 2026 Report, reveals for the first time in history, artificial intelligence has emerged as the number-one healthcare IT investment priority across every single global region tracked outside the United States.

- While execution pressure is mounting, the market remains in an introductory phase, with 37% of organizations prioritizing high-level AI strategy, governance frameworks, and readiness assessments.

- Dictating 57% of emerging technology mindshare, ambient clinical voice technologies have become the primary entry point for software-driven workflows to combat physician burnout.

- Cloud adoption has experienced a massive shift from planning to execution, with 73% of international health networks actively deploying clinical workloads natively across public or hybrid environments.

- Facing extreme economic volatility and budget pressures, concrete plans to engage external consulting firms have plummeted to a four-year low of just 25%.

Global Health Systems Pivot to Targeted Neural Infrastructures

The international healthcare information technology (HIT), ministerial procurement, and clinical operations sectors have broken past a critical historic boundary. For the past several years, global health networks outside the United States approached clinical software overhauls through expansive, multi-million-dollar relational database implementations and generalized system expansions. However, faced with historic labor shortages, severe operational margin compression, and an unprecedented surge in multi-morbidity patient volumes, the traditional IT deployment playbook has been completely rewritten.

According to the KLAS Research Global HIT Trends 2026 Report, which analyzed investment priorities across 182 healthcare organizations spanning 43 countries, the market has officially entered a hyper-targeted era of artificial intelligence and infrastructure rationalization.

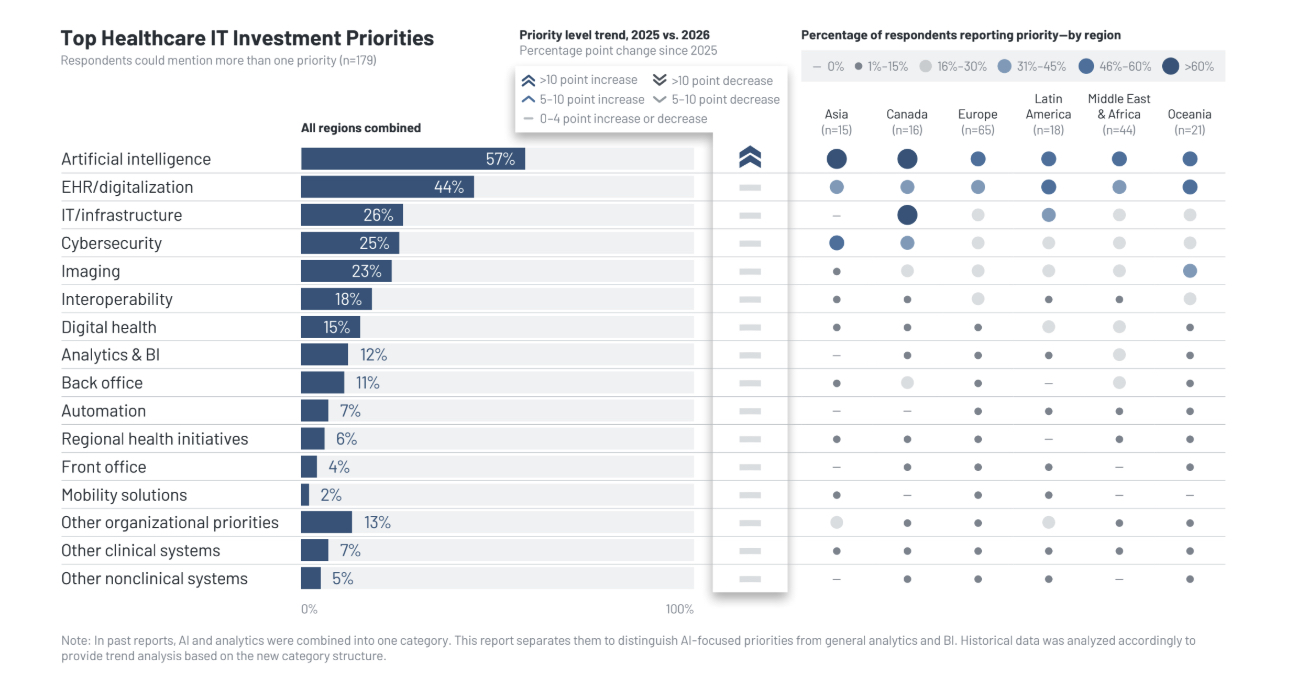

For the first time since tracking began, artificial intelligence has solidified its position as the top technology investment priority in every measured international region, capturing an overall 57% priority rate among global health leaders.

This structural shift signals a deep re-allocation of capital. Hospital boards and regional ministries are freezing generic IT projects to route compressed budgets directly into technologies that promise immediate clinical workflow relief.

This AI expansion is completely changing adjacent procurement layers, driving rapid advancements in database modernization, cloud storage migration, and zero-trust cybersecurity frameworks—all designed to prepare the enterprise foundation to ingest cognitive computing models.

Strategy, Governance, and Ambient Domination

While the pressure to deploy artificial intelligence is accelerating across international boardrooms, the KLAS data reveals that the market is navigating an intensive phase of foundational governance. Rather than deploying uncalibrated black-box tools blindly into active clinical tracks, 37% of organizations are restricting near-term spend to defining core AI strategies, drafting safety frameworks, and executing data-readiness assessments.

Among platforms moving directly into active clinical settings, ambient speech technology commands an undisputed 57% majority of emerging tech excitement. This focus on ambient documentation represents one of the most concrete clinical AI wins achieved by the industry, delivering immediate, quantifiable relief from clerical noise and directly combating physician burnout across Canada, Europe, Asia, and Oceania.

Beyond ambient dictation, 49% of global organizations are aggressively exploring a mix of specialized clinical and operational AI tools. These priorities include diagnostic imaging algorithms for high-acuity stroke, breast, and chest triage (17%), alongside autonomous coding and capacity management agents (16%) designed to optimize throughput without expanding headcount.

The Public Cloud Surge: Moving Past the Data Sovereignty Wall

The rapid deployment of automated intelligence loops has served as a primary catalyst for an unprecedented wave of public infrastructure modernization. Global healthcare cloud adoption has reached an all-time high, with 73% of international organizations now actively leveraging cloud environments within their IT strategy—a major leap over the flat 59% benchmark recorded in 2025.

Historically, strict regional data sovereignty and localized security regulations—particularly across the European Union and the Middle East—forced health networks to rely on complex, expensive on-premises servers or restricted private data silos.

However, as major public cloud hyperscalers have aggressively constructed localized compliance architectures and server farms on sovereign soils, the market has pivoted. Health systems now increasingly view public environments as superior alternatives that deliver the elastic computing capabilities required to process massive neural model workloads.

As these cloud architectures mature, organizations are moving far beyond peripheral storage use cases to migrate core clinical systems of record. Electronic Health Records (EHRs) sit at the absolute forefront of cloud deployment strategies, capturing 37% of active or planned use cases, followed closely by diagnostic imaging networks (27%) and advanced analytics foundations (26%).

Microsoft Azure maintains an undisputed lead, commanding 56% of global mindshare due to its deep integration with pre-existing enterprise productivity suites and single sign-on security frameworks.

Concurrently, Oracle Cloud Infrastructure (OCI) emerged as the only cloud engine to see a net increase in consideration (16%), heavily driven by Middle Eastern and African networks migrating their legacy ERP databases and newly consolidated EHR platforms into integrated Oracle architectures.

The Consulting Contraction: The Rise of Internal Operational Autonomy

The most striking structural pivot documented in the 2026 KLAS report is the severe contraction of the traditional IT consulting pipeline. Under intense macroeconomic pressure to strip out discretionary administrative waste, concrete plans to engage external consulting firms have plummeted to a four-year low of just 25%. In stark contrast, 42% of global healthcare organizations state they have no upcoming plans to leverage external advisory support, choosing instead to protect margins by maximizing internal engineering talent.

This consulting freeze is heavily pronounced in Oceania (60% rejecting external help), Latin America (50%), and the Middle East (48%), where health networks are fiercely rationalizing spending[cite: 3]. This shift is also tied to a profound drop-off in major transactional core database purchasing activity witnessed over the past 24 months, which left fewer massive system overhauls for traditional integrators to manage.

Where limited external expertise is still being utilized—primarily across Canada and Europe—it is restricted to targeted IT advisory services (45%) and implementation leadership (28%) for large-scale digital transformation initiatives.

While legacy firms like Deloitte (22%) and Accenture (13%) maintain top-of-mind awareness for cross-regional strategic planning, 75% of organizations are actively shifting toward niche, localized consulting partners that offer deep domain expertise and less expensive contract models.